Kaya Kinondo Community Bank: a successful mechanism for empowering people

Full Solution

branding the newly completed building

melckzedeck osore

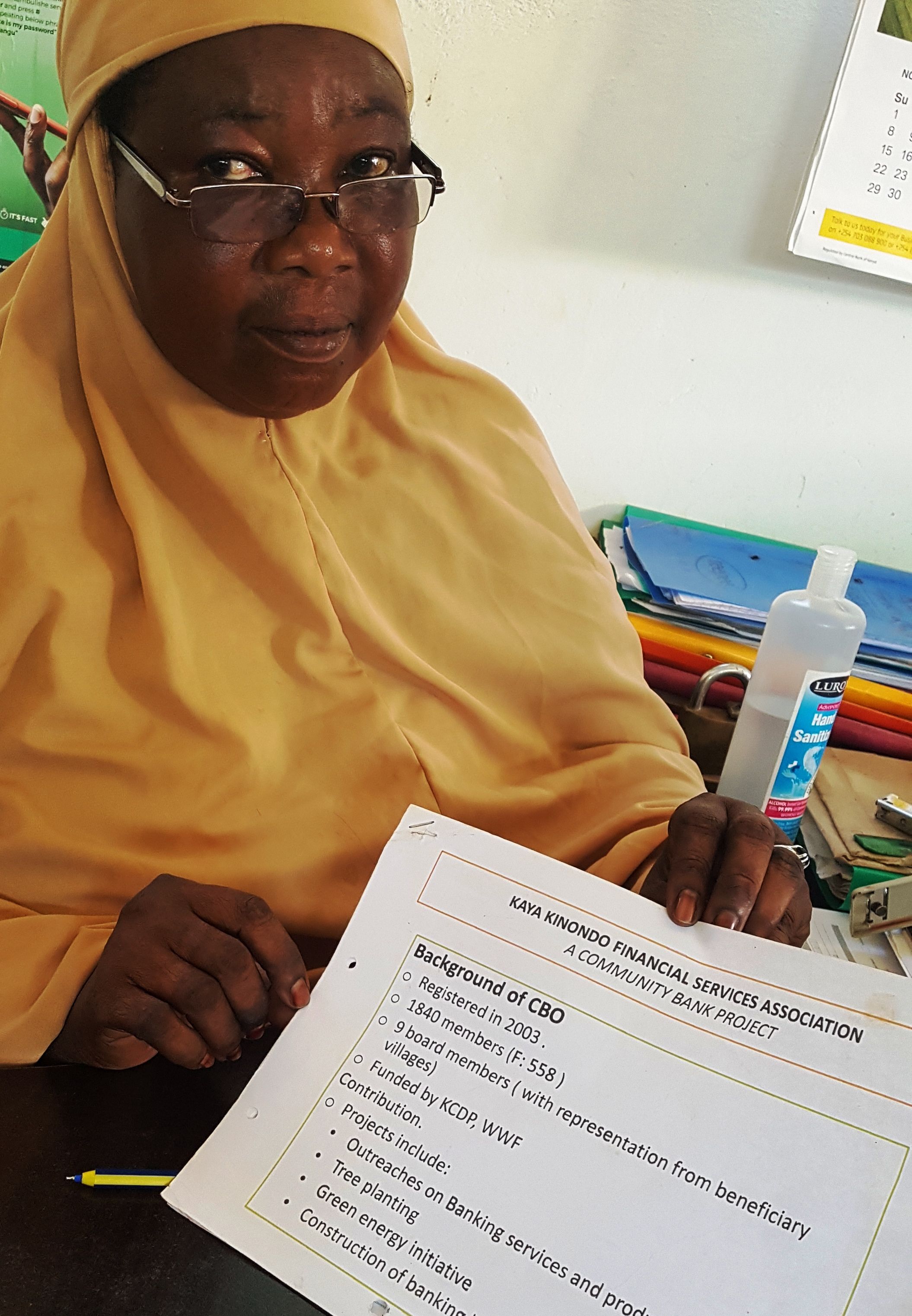

Kaya Kinondo Community Financial Services Association (KKCFSA) was established in 2003. It has over 2,000 members of which more than 25% are women. The Association has previously conducted community outreach on banking services supported by World Wildlife Fund for nature (WWF), National Bank of Kenya and Base Titanium Mining Company. It provides loans at subsidized interest rates to community groups to undertake initiatives that protect the environment and improve livelihoods.

KKCFSA constructed a modern bank to improve effectiveness of providing timely micro credits. The Bank is enabling the community to access favourable loans hence encouraging them to reduce their financial dependency. It is also nurturing community's culture to save profits obtained from their economic activities. In 2016, KKCSA gave out loans of KES 18 million (USD 180,000) to 358 members. It is transforming Kinondoni Village into a modern self-sustaining economy.

Last update: 30 Sep 2025

3611 Views

Context

Challenges addressed

- Unsustainable use of natural resources due to financial dependency on fishing and hand-outs, and the lack of a clearly defined culture of saving profits.

- Limited access to documentation on local environmental resources and their sound management – leading to environmental degradation.

- Initially, high illiteracy rates among the members of the Association and community in general, impeded communication among them, and with partners.

- Instability aggravated by lack of food security due to limited alternative livelihood opportunities.

- Unreliable means of livelihood meant that local people survived from hand to mouth and could therefore not cultivate the culture of saving for a rainy day.

- High interest rates of over 14% by commercial banks prevent local people from accessing loans.

- Raising 10% cash, which was the conditional requirement for all applicants prior to receiving 90% grants from the World Bank fund through the Kenya Coastal Development Project (KCDP).

Location

Kinondo, Kwale, Kenya

East and South Africa

Process

Summary of the process

Collaboration between community and partner organizations e.g. KMFRI, WWF, NBK, Base Titanium, Kwale County and National Government, has been key to ensure KKCSA works like a conventional bank, yet low on interest rates, affordable to all villagers. Above all, the ground was healthy to build on, since leaders have demonstrated the way for the common good, with respect to principles of transparency and rotating board members.

KMFRI has involved the Kinondo community in routine marine and coastal research especially on mangrove and fisheries. WWF has continually offered advice and built staff capacity on various aspects. Base Titanium arranges exchange visits and outreaches activities for KKCSA members to smoothly implement projects by traders, fishers, farmers and others. Members were initially taught banking procedures by NBK. Following devolution of Government, KKCSA now receives direct support from the Kwale County. More financial support comes from improved value chain (selling home made seaweeds products), income from tourism, paid visits by students, grants and from NGOs. Through National Government, it was possible for KCDP to provide HMP grant to construct and furnish the bank.

Building Blocks

Mobilizing Community Members through Local Leaders

Kinondo community recognised the need and importance of coalescing around a common vision in order to attain self reliance and improve their livelihood. They realised that while it is important to retain a strong leadership in the top management of the Bank, it is necessary to rotate members of the Committee regularly to enable members to introduce new ideas. The opportunity is available for any capable individual to join the leadership committee. This is done democratically by holding regular elections. In order for the bank to thrive, Committee members are encouraged to create awareness and to encourage local people and those from the wider Msambweni Ward to join KKCSA to save and obtain loans and related services.

Enabling factors

- Community share common values in culture, faith and tradition, and they are also affected by similar challenges.

- Goodwill from the community living in Msambweni Ward and its neighbourhood.

- Community engagement and empowerment.

- Bank covers multiple needs for all categories of the local people.

- Limited inclusion and involvement of political sentiments.

Lesson learned

- Knowledge of the local languages, culture and tradition is crucial for implementing processes.

- Delay in approval processes is caused by limited number of experts from relevant departments in the County and National government.

- Inclusion of the community project in the annual County Integrated Development Plans (CIPD) contributes substantially in ensuring project sustainability.

Resources

Capacity building on financial management

Committee members were trained on book-keeping, basic audit process, budget planning and selection of tenders for constructions. Using partners such as the National Bank of Kenya (NBK) to train new committee members and regularly provide refresher courses for existing members has been essential to enable the Bank to grow more independently, save cost, and retain modern banking operations. Youth, especially local students, were involved to assist in drafting proposal writing and record keeping, applying what they learn at school.

The Association members were trained on writing and submitting applications for World Bank funding through HMP, which is critical for future funding or to obtain development loans. They also learned to develop their Strategic Plan 2018-2022. This strategic planning has enabled the Association to have clear focus of where they want to go. Although., there is need to start developing a new Strategic Plan for the next cycle, where partners including Base Titanium, relevant County Government department and NGOs operating in the area can be mobilised to assist in the process.

Enabling factors

- Capacity building and infrastructure support has been provided by partners.

- The need to have a local bank nearby in order to reduce the cost of travelling long distance for banking.

- Opportunity is being created for local students and youth to appreciate banking as a profession and to consider it as a career in the future.

- Obtaining loans no longer require a laborious process with long distance travel to a major town such as Kwale or Mombasa.

- The County Government can now channel funds more effectively and fast to the local Community Cased Organizations via KKCSA.

Lesson learned

- Training of Trainers - Use locally built capacity to train others and replicate projects in the neighbouring communities.

- When trainers emerge from among the community following effective capacity building campaigns, they are appreciated locally and emulated easily.

- Knowledge learnt in various aspects of financial management and banking opens up new career possibilities for the young, which were previously obscure such as book keeping, of foreign such as Information Communication Technology (ICT).

- Locally nurtured capacity through training of trainers is more effective because the lessons can also be conducted in the local language.

Partnership strengthens stakeholder linkages for Sustainable Growth

Partnerships with KMFRI and other relevant county departments have enabled the proposal development by the association to be review regularly and more effectively in order to submit a clear and non-ambiguous proposal to the World Bank and other funders. Handholding by partner agencies such as KMFRI, WWF, National Bank, Base Titanium, etc. has been essential in enhancing the knowledge on tendering, procurement of construction material, furniture and equipment.

Enabling factors

- Recognition that the project is addressing the need of the entire community.

- Presence and participation of stakeholders from various sectors is providing effective technical knowledge and know how, as well as opening career opportunities for the youth.

- Participation of community members in the activities of various stakeholders is creating job opportunities.

Lesson learned

- Appropriate timing for engagement of the local communities is crucial for success – the day, place and time of engagement must be agreeable to all otherwise the partnership will be skewed and might appear to be imposed.

- Respecting and appreciating community culture and traditions is critical for smooth implementation of project activities e.g. ceasing to work during prayer time, or rescheduling to attend meetings (Known as Baraza) hosted by area Chief or Government representatives.

- Culture of saving part of the income earned from daily activities is possible through discipline and good planning.

- Antagonizing the community against fellow partner agencies should be avoided at all time.

- All partner agencies working with the communities must stick to their roles and responsibilities at all time.

- Sustainability of the community project is the most crucial aspect that will ensure the project doesn’t collapse once the champions exit or move on. New members must therefore be recruited constantly and trained on the ideals of the project through an internship programme.

Impacts

- The financial independence has enhanced the resilience of the local people in times of crises e.g. during drought, the COVID-19 pandemic. The bank is diversifying services by offering loans to purchase bicycles and motorbikes in the thriving transport sector.

- Livelihood of the local community is thriving because people can reliably obtain soft loans to invest in fishing, agriculture, tourism, co-management of forests and cultural sites.

- Enhanced saving culture of the people and improved infrastructure in Kinondo and the wider Msambweni Ward adjacent areas.

- Defaulting loan repayment is drastically minimised because issuance is usually through groups of shareholders who guarantee one another. Therefore, group members comes to the rescue of another to avoid defaulting.

- Literacy rates have risen drastically due to the improved livelihood of the community enabling them to secure affordable loans for paying school fees timely and regularly.

- Youth are gaining practical experience and knowledge in the banking sector. Plans are also underway to diversify clients by targeting the youth.

- Empowerment of the people of Kinondo and its environs.

- Plans are underway to replicate the bank in the neighbouring sub-county of Lungalunga.

- Through partnership with BaseTitanium, an Memorandum of Undertanding (MoU) has been developed to target farmers in order to increase diversity of membership base

Beneficiaries

- Individuals benefiting from loans.

- Community based organizations, Women and Youth Groups.

- Vulnerable and Marginalised Groups and Persons living with disabilities.

- Traders, fishers, farmers, employees in various sectors.

- Community run schools.

Sustainable Development Goals

SDG 1 – No poverty

SDG 5 – Gender equality

SDG 8 – Decent work and economic growth

SDG 9 – Industry, innovation and infrastructure

SDG 14 – Life below water

SDG 15 – Life on land

SDG 17 – Partnerships for the goals

Story

Joining modern knowledge from the youth with experience from elders

The community of Kaya Kinondo Village had a dream to progress in life and live a better, more fulfilling existence than their ancestors. Located within the touristic south coast area of Kenya, village people mainly obtain their livelihood from fishing, small scale farming, guiding tourists on the beach, trading, cutting mangroves and entertaining tourists in the beach hotels. They used to meet every evening under a tree to pool together their daily earnings. Once in a while, a member would borrow from the savings and repay when convenient. They realised that meeting under a tree was risky and unsustainable. So, they saved enough money to build a small house, which they called their Village Bank. Although the savings improved, this situation was still unsafe, and members had to carry home the collected money each evening.

In 2014, they heard about the Kenya Coastal Development Project (KCDP) funded by the World Bank and Government of Kenya. KCDP had a component known as Hazina ya Maendeleo ya Pwani (HMP), which funded community projects. They approached HMP with a proposal for a lasting solution - to build a modern village bank that would serve them and all community projects operating in the Kinondo Village and, eventually, the entire Kwale County. The youth, with their contemporary knowledge acquired from school and the elderly members with long term personal experience from their various occupations produced a proposal to build a self-sustaining modern village bank. The bank is transforming Kinondoni into a modern self-sustaining economy, which in 2016 gave loans of KES 18 million (USD 180,000) to 358 members. The youth have assisted in developing a strategic plan that aims to upgrade the bank into a Savings and Credit Cooperation Organization (SACCO).

This illustrates how a village economy upgraded from the shed of a tree, into a house then eventually to a modern bank, with the hope to transform into a SACCO.

Connect with contributors

Other contributors

Ms Farida Hassan

Pwani University, Kwale, Kenya

Mr. George Morara

Kisii University

{kind=link}

{kind=link}

{kind=link}

{kind=link}